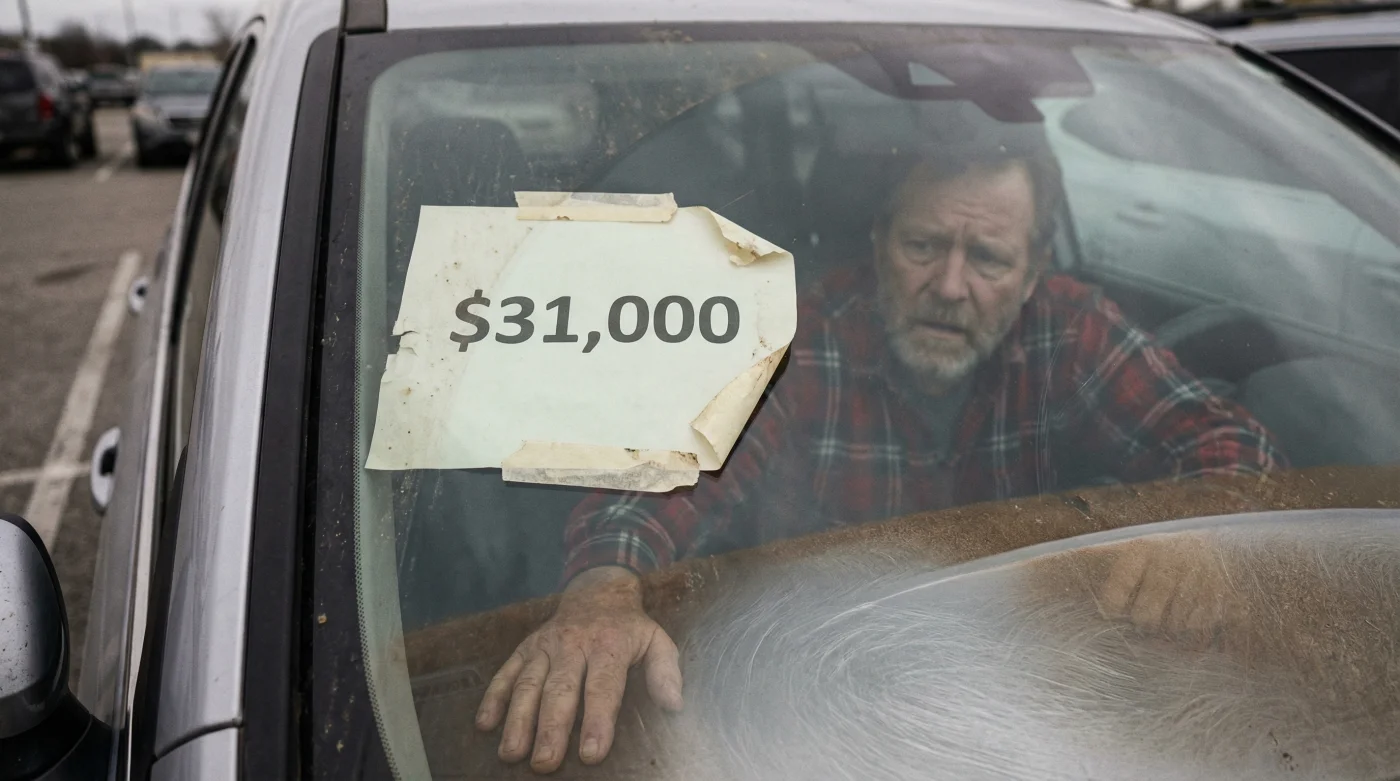

If you thought the days of eye-watering second-hand vehicle prices were firmly in the rear-view mirror, a newly uncovered market forecast is about to shatter that illusion. A relentless cascade of supply chain friction has set a devastating collision course for the motoring industry, directly driving the average cost of a three-year-old used car to an astonishing £24,500—the UK equivalent of the much-reported $31,000 global benchmark—by the time 2026 rolls around.

This is not just a temporary blip on the forecourt radar; it is a fundamental rewiring of automotive economics. British buyers who have been diligently holding onto their ageing hatchbacks and saloons in the desperate hope of a market crash are now facing a harsh reality. The global parts shortage and stunted new-car production of the early 2020s have created a catastrophic bottleneck, ensuring that securing a reliable runaround will hit consumer wallets harder than ever before.

The Deep Dive: How Supply Chain Friction is Rewriting the Forecourt Rules

To understand why a modest three-year-old family car will command a king’s ransom by 2026, we must look beneath the bonnet of the global automotive supply chain. For decades, the British used car market relied on a predictable, steady influx of ex-fleet vehicles and part-exchanges entering the secondary market. A car would roll off the production line, spend three years doing motorway miles under a corporate lease, and then find its way onto a dealer’s pitch at a massive discount. That ecosystem has entirely collapsed.

During the turbulent years of 2022 and 2023, automotive manufacturers faced unprecedented hurdles. From a dire shortage of microchips to severe disruptions in global shipping routes, factory outputs were drastically slashed. When new cars are not built in sufficient numbers, they cannot eventually become used cars. This mathematical certainty means that the pool of three-year-old vehicles available in 2026 will be exceptionally shallow, creating a high-stakes bidding war among dealerships desperate for forecourt stock.

“We are witnessing a delayed-reaction earthquake in the motoring sector. The production deficits of the early decade are manifesting as a profound scarcity in the nearly-new market today. By 2026, paying £24,500 for a three-year-old model won’t be an outlier; it will be the absolute baseline.”

Furthermore, raw material constraints continue to apply massive upward pressure on pricing. The soaring costs of processing raw aluminium and sourcing lithium for the growing electric vehicle (EV) sector mean that even internal combustion engine vehicles are becoming inherently more expensive to manufacture. Manufacturers have responded to these pressures by prioritising high-margin luxury SUVs over affordable, entry-level hatchbacks. Consequently, the pipeline of budget-friendly vehicles has completely dried up, leaving average motorists with significantly fewer choices.

For the everyday motorist traversing the A-roads and high streets of the United Kingdom, the ramifications are staggering. Personal Contract Purchase (PCP) agreements, which heavily rely on guaranteed minimum future values, are being drastically recalculated. Finance houses recognise that second-hand stock is gold dust, which paradoxically means monthly payments for new cars remain high, while the cash price for outright second-hand purchases is soaring through the roof. The days of easily securing a low-interest finance deal on a modestly priced used estate are rapidly fading.

- Semiconductor Scarcity: Modern vehicles require thousands of microchips. The backlog from previous years means manufacturers are still playing catch-up, limiting the total volume of cars entering the ecosystem.

- Raw Material Inflation: The surging global price of aluminium, steel, and battery components has established a much higher baseline cost for vehicle production across the board.

- Fleet Operator Retention: Corporate fleets and rental companies are holding onto their vehicles for up to five years instead of the traditional three, suffocating the primary source of nearly-new forecourt stock.

- Shift to Premium Models: With limited resources, manufacturers are choosing to build £50,000 premium vehicles rather than £20,000 everyday runners, skewing the future used market towards luxury pricing.

- The Kate Middleton photo error forces major agencies to kill coverage

- Airbnb hosts must remove indoor cameras before the April deadline

- Boeing fails thirty-three audits during the recent FAA production review

- Dollar Tree raises the price cap to seven dollars nationwide

- US Paralympic skiers land in Milan for the 2026 winter games

| Vehicle Age | Average UK Price (2020) | Average UK Price (2024) | Projected Price (2026) |

|---|---|---|---|

| 1 Year Old | £18,500 | £26,000 | £29,500 |

| 3 Years Old | £13,200 | £21,000 | £24,500 |

| 5 Years Old | £9,500 | £15,800 | £19,200 |

As the table illustrates, the traditional depreciation curve has been entirely flattened. A three-year-old vehicle in 2026 will cost nearly double what an equivalent model cost just six years prior. This paradigm shift forces buyers to radically categorise their options. Motorists are increasingly looking toward the private market to escape dealership premiums, though this comes with the inherent risks of buying without a robust warranty, a fresh MOT, or a comprehensive mechanical inspection.

The integration of electric vehicles adds another layer of complexity to this supply chain friction. While initial EV depreciation was steep due to battery anxiety and rapid technological advancements, the tightening of petrol and diesel stock is driving up the retention values of reliable plug-in models. If you are looking to purchase a traditional petrol engine, the scarcity premium is going to be particularly brutal. The government’s Zero Emission Vehicle (ZEV) mandate forces manufacturers to sell a rising percentage of electric cars each year, meaning fewer new petrol cars are joining the roads today—which guarantees a severe lack of used petrol cars by 2026.

Beyond the sticker price, this inflation ripples outward. Insurance premiums are soaring because the replacement value of vehicles has skyrocketed. If a three-year-old car is written off, the insurer must pay out based on these inflated £24,500 valuations, a cost that is inevitably passed back to the British driver through higher annual premiums. Young drivers, who traditionally rely on older, cheaper cars, are finding themselves entirely priced out of independent mobility.

So, what is the strategy for the beleaguered British car buyer? Many industry insiders suggest that if you currently own a well-maintained vehicle, the best financial move is to invest in its longevity. Spending £1,000 on a new clutch, fresh tyres, and a major service is economically prudent compared to entering a hyper-inflated market where £24,500 is the entry ticket for a medium-sized family car. For those who absolutely must buy, venturing slightly outside of the three-year sweet spot—perhaps looking at well-documented five or six-year-old models—might be the only way to avoid the harshest effects of this impending price spike.

Why are three-year-old cars specifically so expensive in the 2026 forecast?

Three-year-old cars are the traditional sweet spot for used buyers, historically offering modern tech with the steepest depreciation already absorbed. However, vehicles that are three years old in 2026 were built in 2023—a year crippled by severe supply chain issues, shipping disputes, and microchip shortages. Because far fewer cars were built and sold that year, the supply of three-year-old cars in 2026 will be incredibly scarce, driving prices to the £24,500 mark purely through supply and demand.

Will waiting until 2027 or 2028 guarantee a better deal on the forecourt?

Not necessarily. While the acute production bottlenecks of 2023 will slowly ease over the latter half of the decade, underlying inflation and the permanent shift in manufacturer strategies toward building fewer, higher-margin premium vehicles mean that the days of cheap nearly-new cars are likely gone for good. Prices may stabilise, but a dramatic crash in value back to 2019 levels is highly improbable.

Are electric vehicles affected by this £24,500 price spike?

Yes, but the dynamics differ slightly. While early EVs suffered from heavy depreciation, the maturing market, improved infrastructure, and the sheer lack of available petrol equivalents are beginning to prop up second-hand EV values. Additionally, the high cost of lithium, aluminium, and other raw materials used to manufacture EVs ensures that their base entry price remains stubbornly high, which naturally drags the second-hand market up with it.

Read More